Modified Duration in Semi-Annual periods converted to Annual

Why is it that to convert a Semi-Annual Modified Duration to an Annual one, we divide by 2 instead of multiplying by 2? Surely it doesn’t imply that the bond price will move more in half a year than in one full year when interest rates shift?

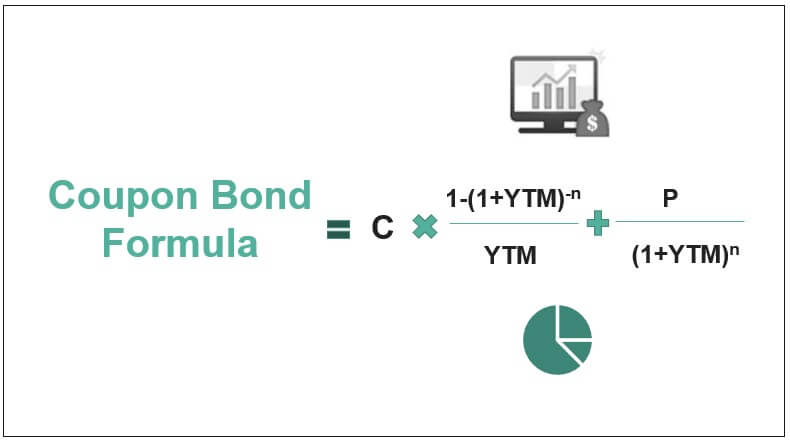

Coupon Bond Formula - What Is It, Calculation, Examples

Modified Duration of semi annual coupon bond

Calculate The Price Of A Bond With Semi Annual Coupon Payments In Excel

Modified Duration vs: Macaulay Duration: Key Differences - FasterCapital

Duration and Convexity, with Illustrations and Formulas

Zero-Coupon Bond Formula + Calculator

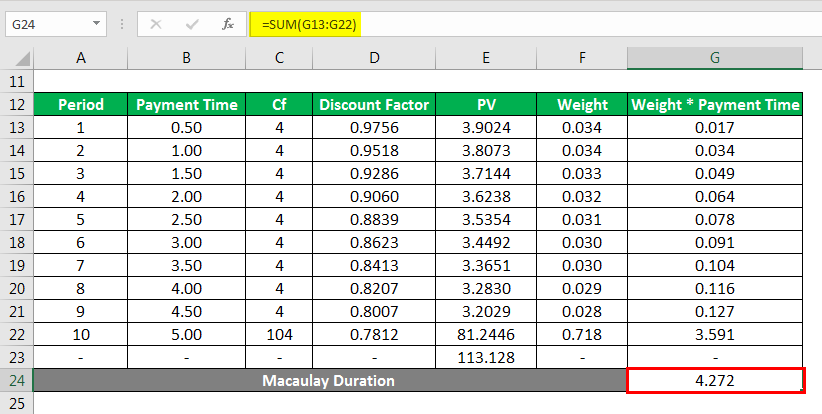

Macaulay Duration of a Semi annual coupon bond

Yield to Maturity (YTM)

Modified Duration Explanation, Example with Excel Template

Mastering Bond Duration with Weighted Average Life - FasterCapital